In this article, we're going to cover four ways to calculate the value of a company:

- The Asset Valuation Method

- The Entry Cost Method

- The Earnings Multiple Method (also known as the Price / Earnings or P/E Ratio)

- Discounted Cash Flow Method (DCF) - the professional's approach

First though, let's imagine you're the luck winner of the $202m jackpot in the New Jersey lottery (which happened in February 2020).

The lottery board offers you a choice. You can have a lump sum of $142.2m payable immediately. Or you can get 30 annual payments. Each year's payment is 5 percent larger than the previous one and you'll get a total of $202m over the 30 years.

Which option would you choose? And why?

Strangely enough, the New Jersey Lottery Board doesn’t care which you choose

It’s going to cost them $142.2m no matter what. They’ll either give you the lump sum, or they’ll give a finance company the lump sum and the finance company will then make the 30 annual payments to you. In other words, the NJ lottery are saying those 30 future payments totalling $202m are worth $142.2m in today’s money.

Determining the value of a business takes a similar approach

Regardless of whether you're a small business or a large coroprate, to calculate the value of your business you need to determine the price, in today’s money, of buying the future cashflows generated by your company.

Before explaining how to do that, I’m going to share two basic methods that can be used to benchmark what someone is willing to pay. Then I’m going to share the simple rule-of-thumb method for valuing a business.

The remainder (and bulk) of this article is about the three questions that corporate financiers and savvy investors ask themselves when valuing a business, the technique they use to calculate the value (with worked examples) and it finishes off with a story about how a savvy entrepreneur used this knowledge to sell her business for an outrageous premium.

Let’s start by looking at two ways of creating a benchmark value for your business.

Benchmark Valuations

How to value the assets in your business

The minimum you could expect to receive is the market value of the assets owned by the business. This is effectively the closing doing value. This sometimes happens because you can't find a buyer for your business because:

- You (the owner) are is the driving force behind the business and without you being there it will fall over (click here to discover the 9 warning signs that this could be you!)

- It’s in a dying industry or they haven’t invested to keep up with the competition

- It has a bad reputation in the industry

- There are significant risks such as outstanding warranties, lots of bad debts or large creditors

Basically, the business isn’t considered to be a going concern

When they buyer decides the business isn’t a going concern, they're only interested in buying the assets of your business. So, the value becomes what you can get from selling things like land, buildings, stock, plant, and machinery. Start with the net book value showing in your accounts, and then adjust for market conditions and be realistic about what you can achieve.

However, If your business has more value as a going concern (ie: there’s value from keeping it trading), then the buyer needs to determine which is better for them: buying your business or creating a new one from scratch? Which is where the Entry Cost method enters the fray.

How to calculate the market entry cost

This is the lesser known of the four approaches, but it is the top price a buyer will offer for your business. Before making an offer, EVERY acquirer will ask themselves “Should we build this ourselves, or should we buy it?”, and they start with...

How much it would cost us to build this business?

They’ll evaluate the costs of purchasing physical assets, recruiting and training people, creating the intellectual property, developing the technology, and the advertising and marketing costs of building the customer base. They’ll estimate how long it will take to get this business to the point where you’re at now. And they’ll calculate how much money they’ll lose in the time it takes to do that.

Those things together tell them what their top limit is for buying a business like yours. If you want more than what they believe the entry cost is, they’ll not buy you. They’ll do it themselves.

But you can also use this knowledge to your advantage

When evaluating an offer, put yourself in your prospective acquirer's shows. Estimte the time and cost it would take the buyer to enter the market without you. You can leverage that knowledge to highlight the risks and costs of the buyer doing it themselves. Allow you to negotiate towards that top number and get the best price possible.

Which is what Rod Drury did when he sold his business

Rod’s business, Aftermail, provided an email archiving software solution that enabled Fortune 500 companies to meet the legal requirements of the newly introduced Sarbane-Oxley act in 2002.

Aftermail had only two customers and $2m in revenue when Quest Software bought them in 2002. But Quest paid $45m for the privilege of owning Aftermail!

Why did they pay so much?

Well, Quest sold software to all the Fortune 500 companies, but it was losing market share to competitors who had an email archiving solution. Rod knew it would take them about two years to get to market. He knew they had to recruit and build a team to develop and test an email solution he knew they couldn’t guarantee what they built would work. Whereas he had ap proven system with customers. So, Quest decided that paying $45m was a cheaper, faster, and lower risk option than doing it themselves.

Let’s move on now to the approaches you’ll hear talked about most often, which I call the ...

Future Value Calculations

How to Value a Business Quickly: The Price / Earnings Ratio

The price / earnings ratio (P/E) or earnings multiple method is used to value more established businesses. This is how you value a business based on profits. If you look in the financial sections of newspapers, you can see the historic P/E ratio for listed companies. It’s the same thing as multiple of profits. As in “what multiple of profits did you get when you sold?”

For example, if you made £300k pre-tax profit last year and you’re offered a P/E ratio of 4, then the buyer is valuing your business at £1.2m.

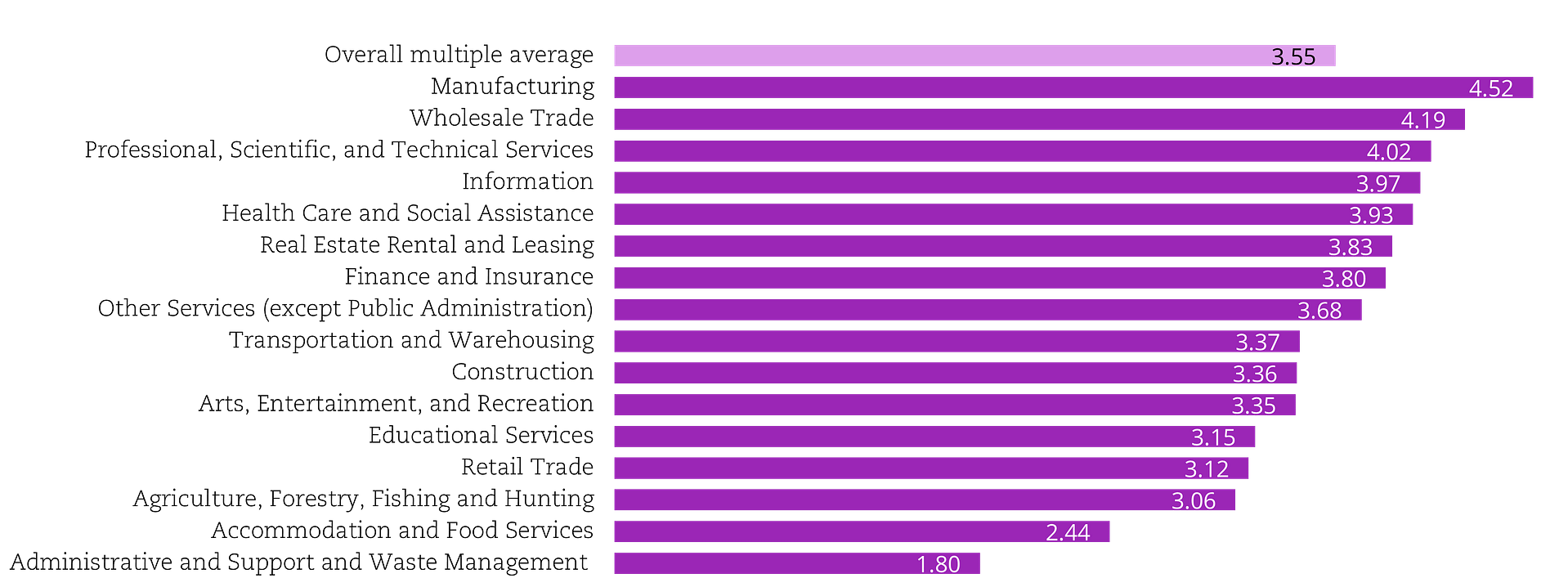

There are certain rules of thumb used to determine the multiple

Bigger companies tend to get higher multiples. High growth companies get higher valuations than mature companies. Companies listed on stock exchanges get higher multiples than unlisted companies. Different industry sectors attract different multiples as you can see below:

Based on Value Builder anlaysis of the offers recieved by 71,000+ companies, the average offer is 3.55 times profits, varying from 1.8 times for admin and support up to 4.52 for manufacturing

You can use this method to quickly estimate the value of your company. It's a great benchmark valuation.

We move now from multiple of profits to our final method, which is based on the estimated cash your business will generate in the future and how much that’s worth in today’s money...

How to value your business using discounted dashflow analysis (DCF)

This is the approach that corporate financiers and savvy investor use to value your business. It's technical and the calculations can be confusing. What the investors are really trying to do is answer three fundamental questions:

- What cash might this business generate in the future?

- How reliable are those estimates?

- What's it worth in today’s money?

Let’s work through those to see how they impact the value of a business.

What cash might this business generate in the future?

The industry term for this is the future free cash flow (FCF). It’s the money that can be extracted from the business and distributed to creditors, lenders, and shareholders without affecting the company’s operations. For most smaller businesses, it’s typically the money you have available to pay dividends and pay down loans. You can read more about the detailed calculation here if you’re interested.

What do they look at?

They’ll be considering your history and how steady your FCF was, and they ‘ll look at your growth potential. They’ll ask questions like: Are they sailing with or against the wind? How big could this business get? What would it cost to scale it up? (Click here for articles on growth potential)

How reliable are those estimates?

They’re going to dig into all the risks associated with your business. Things like how dependent the business is one any single employee, supplier, or customer. Whether you have recurring revenues (see here for more on that), and how engaged your employees are (see here for articles about building an engaged team).

The biggest risk for a prospective investor is the business’s dependence on You! The more dependent your business is on you the greater they buyer's risk.

What’s it’s worth in today’s money?

The assumption here is that the value of money today is worth more than the value of money tomorrow. So, your buyer will calculate the value of your future free cash flows in today’s terms based on the returns they want to get to compensate for the risk involved. Hence the name discounted cashflow analysis – they're going to discount the amount the pay for that future money because of things like inflation, cost of borrowing, and the uncertainty of not getting it. The name for future money calculated at today’s value is called the “present value”.

How’s present value calculated?

Imagine you had £100k today, and the bank paid you a 10% annual return. At the end of year 1, you’d have £110k. At the end of year 2, you’d have £121k, and at the end of year 3, you’d have £133.1k. In other words, £133.1k payable in three years’ time is worth £100k in today’s money based on a 10% per annum return.

When working backwards from a future amount, we rename the expected return as the discount factor, and the calculation becomes:

Value in Future / ((1+discount factor)^(number of years ahead))

Using our example above, the 3-year value is £133.1k, and the discount factor is 10%, and the calculation becomes:

133.1k / ((1.15)^3) = 133.1k / 1.331 = £100k

Which can all be a bit confusing if you’ve never seen the theory before. So, let me explain with some examples…

Calculating Your Business's Value Using DCF

We’re going to use the DCF methodology to look at how growth and risk affect the valuation of a hypothetical business to help explain the concept...

Scenario 1: No Growth and Low Risk

Let’s assume your company is going to generate £1m per year of free cashflow for the next 10 years, and the buyer wants a 15% return on their investment.

The present values of those future cashflows are calculated for each year. The sum of those values (the net present value) is what the buyer would be willing to pay you for those future cashflows.

In this example, your business would be worth just over £5m.

Scenario 2: No Growth but High Risk

Let’s assume your company is still going to generate £1m per year of free cashflow for the next 10 years.

But this time, imagine the prospective buyer looks at your business and thinks “Hmm, this is a really risky business. I’d need to be getting a return of 50% a year to take on that risk". (Yes, that seems high, but it’s not unusual for venture capital funds or private equity houses).

In this example, your business is worth just less than £2m to the prospective buyer. That's a lot of value lost because the buyer is worried about the reliability and achievability of your forecasts.

Scenario 3: Steady Growth and Low Risk

Let’s assume you've got a great growth plan for the business and that your freecashflow is going to grow by 20% per annum. At the end of the first year, you’ll have £1.2m of free cashflow, and the year after £1.44m and so on.

Imagine, too, that the prospective buyerafter digging round beneath the bonnet of your business, agrees with you and decides that it’s low risk and they only need a 15% return for their investment in your business.

Now we're cooking on gas (as the advert used to say). In this example, your business is worth nearly £13m the prospective buyer. That's a lot of value lost because the buyer is worried about the reliability and achievability of your forecasts.

To recap, your business could be worth anywhere between £2m and £13m depending on its future growth potential and the confidence the buyer has in your numbers.

How to increase your business's potential value so you get a higher price

There are 8 factors that determine your company value. How well you’re scoring on these value drivers are the difference between getting £2m or £13m, and they can make your business irresistible or untouchable for a prospective acquirer . Discover them here: Introducing The Eight Drivers Of Company Value. (You’ll need to sign in to access the videos and transcripts). Let me tell you the story of Stephanie Breedlove and how she leveraged this knowledge to sell her business for an outrageous premium…

Stephanie Breedlove was a new mom and an up-and-coming associate at Anderson (the consulting firm).

She wanted to go back to work so she hired a nanny to take care of her son. Given her job and her husband’s job, they needed to make sure they followed the rules when paying their nanny and be completely legal. She didn’t want to do it herself, so she called some of the big payroll providers. Her calls were rerouted many different times within the call centres. It became clear to Stephanie that no-one was interested. They weren't set up to help one woman in Texas pay her nanny.

The experience was so bad for Stephanie she created her own company

She left Anderson and created Breedlove and Associates to do payroll for nannies. Her company wasn’t Apple, Google, or Tesla. It wasn’t an industry juggernaut. It was a slow-and-steady wins the race type of company. Over twenty years, she built her company up to $9 million in annual revenue, over 20 years.

She sold her little payroll company for a whopping $54 million

It's almost unbelievable. How did she do that? Well, she approached Care.com. Care.com has seven million subscribers. Many of whom are parents with nannies. If fact, if you go to Care.com, you can plug in your zip code (it’s a US company) and it will generate a list of parent-rated nannies that you can hire to take care of your kids.

Breedlove had 10,000 customers on her $9 million of revenue

She argued to Care.com that if only 1% of their 7 million subscribers bought Breedlove’s payroll service, the business would immediately add $63m in revenue, and could easily to grow to be a nine-figure revenue business.

From Care.com’s perspective it was a low-risk opportunity

Breedlove and Associates had a high Value Builder Score (which indicates high growth potential and low risk). The risks were low for Care.com because the business didn’t need her to be there. The processes and systems were all set up and running smoothly. There was a good team in place. It was 100% recurring revenue, and there was a very small churn rate. Hence, the $54m valuation. (You can get your free Value Builder Score here to see how valuable and sellable your business is).

Now for a quick recap of what we've covered …

Summary

There are four approaches to calculating the value of a business:

- Determine the market value of the business’s assets (Asset Valuation)

- The amount of money and time it would cost for an acquirer to build a business like yours (Entry Cost)

- A multiple of your profits, using a rule of thumb for your sector and your company size (P/E ratio)

- The net present value of your future free cashflows (Discount Cashflow Analysis)

If your business has more than £250k EBITDA and you want to sell it as a going concern, then you should expect a buyer to use the Discounted Cashflow Approach when they value your business.

If you are considering selling, you should use the same approach. Start by getting your valuation and your Value Builder Score. You’ll quickly find out how sellable and valuable your business is today, and you’ll understand what work is required to be able to sell it for the price you want. You can get your free assessment here: Get Your Value Builder Score Now

I know this has been a long read, but I hope you’ve not forgotten that you won that lottery earlier! Now you know how to calculate the current value of future income streams, you should be able to make a more informed decision about whether to take the lump sum or the annuity. I know which one I’d be going for  .

.

Warmly

Richard

PS: And finally...

The Reality of Valuing Your Company

Valuing your company is like valuing your favourite Top Trump card or your car : each one is unique and is only worth what someone else is willing to pay for it.

To properly value your company, you need to look at it through the eyes of a prospective buyer, and understand the multiple they will use for your company.

When you sell your car, buyers check for rust and damage to the body work, and check the tread on the tyres. They open the bonnet to look at the engine. They start the car, and take it for a test drive, push every button, flick every lever.

Buyers will check your business in a lot of detail too before they part with their money.

The data we've collected from the acquision offers made to the 80,000+ users of the Value Builder System shows there are 8 attributes that buyers check closely, and are willing to pay a premium for.

Based on our quantitative research of over 80,000 businesses, achieving a Value Builder Score of 80+ will make your company 71% more value than an average business with the same EBITDA

Join 80,000 other savvy owners, and get your Business Valuation Score now to discover:

- How well you're performing in each of the eight areas

- How your company compares against others from your sector

- How much your company is worth today

- How much your company could be worth if you improve your Value Builder Score.

Click on the big button below to get your score now (it only takes about 13 minutes).